债券看成底层财富,赋予奉赵券基金最澄莹的底色。也恰是名字中的“债券”二字,在一定进程上局限了投资者对债券基金在财富建立中饰演何种扮装的思象空间。债券基金该不该配、该配若干等问题,也成为了困扰不少投资者的一个贫乏。今天,就让诺德基金带注庞杂投资者们来聊一聊,在财富建立中,该若何去阐扬债券型产物的多元化上风。

藏身财富建立运筹帷幄,匹相助适的债券型产物

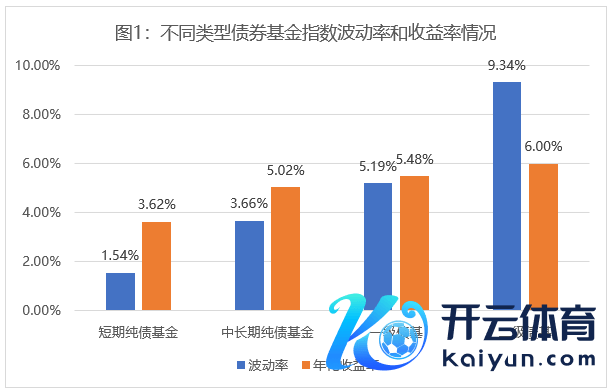

领先,从风险收益组成的“光谱”上,咱们不错看出,不同类型的债券型产物常常贮蓄着不同的风险收益特征。

数据开端:wind,统计区间:2014.01.01-2023.12.31。注:短期纯债基金取短期纯债型基金指数(885062.WI),中恒久纯债基金取中恒久纯债型指数(885008.WI),一级债基取羼杂债券型一级指数(885006.WI),二级债基取羼杂债券型二级指数(885007.WI)。指数行情走势不预示其异日阐扬,也不代表具体基金产物阐扬,基金有风险,投资需严慎。

要是是站在投资者合乎性的角度开拔,那么庞杂投资者在进行财富建立时,不妨不错从以下两方面入部属手,去选用该匹配何种类型的债券。

一、风险收益方面

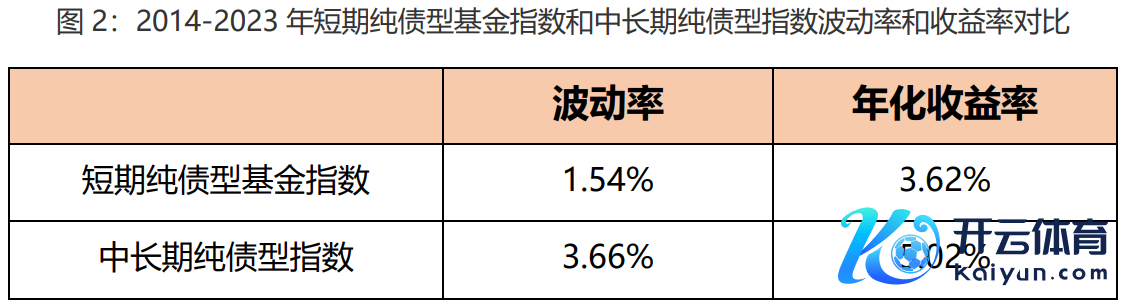

要是投资者追求较低风险和较低收益,那么不错研讨以建立短债基金为主,因为其底层债券的久期较短,诚然举座收益率低于长债基金,但胜在波动相对较低。

图2:2014-2023年短期纯债型基金指数和中恒久纯债型指数波动率和收益率对比

数据开端:wind,统计区间:2014.01.01-2023.12.31。指数行情走势不预示其异日阐扬,也不代表具体基金产物阐扬,基金有风险,投资需严慎。

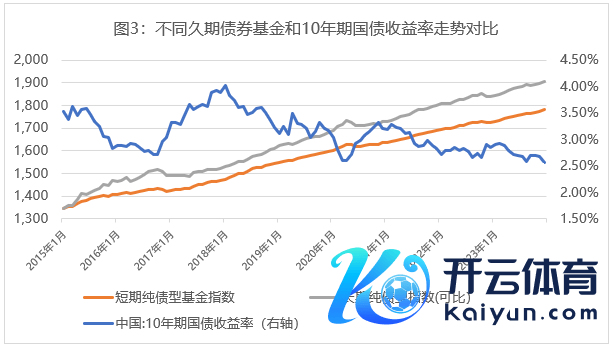

要是对风险和收益的预期皆较为适中,并追求一定的组合隆重性,那么不妨不错研讨将短期要用的资金建立在短债型产物中,而将恒久“闲置”的资金建立在部分长债型产物中。因为其底层债券的久期更长、报酬率也相对更高。诚然就怕会跟着市集利率的变化出现一定的波动,但拉万古分来看,预期收益率也相对可不雅。

数据开端:wind,统计区间:2015.01.05-2023.12.31。指数行情走势不预示其异日阐扬,也不代表具体基金产物阐扬,基金有风险,投资需严慎。

要是投资者不错承担一定的风险,并渴望追求较高的预期收益,那么不错在我方的组合中去进步一定的股票类财富比例,并同期将“含股量”较高的一级债基、二级债基一并纳入研讨鸿沟。

二、投资期限方面

要是投资者的投资期限较短,对握有期间的净值波动容忍度相对较低,那么不错研讨将资金建立在部分久期较短的超短债基金上。而那些久期较长的债券基金,尽管在到期时不错赎回,但它们的净值在短期内可能会也出现一定的波动。诚然恒久握有盈利概率会渐渐提高,但这对投资期限有着更高的条目。从下图中咱们不错看出,不同债券型产物获取100%正收益的最短握有期限连续亦然不同的:

图4:近十年任性时分买入各样债券基金指数握有不同周期获取正收益概率统计

而关于购房这些更为长久的投资运筹帷幄,投资者不妨研讨去建立部分久期较长的中恒久纯债基金,或是股票比例较高的一级债基、二级债基,或者率皆会是比较合适的选用。数据开端:wind,统计区间:2014/1/1-2023/12/31。注:统计上述时分区间任性一个来去日买入基金指数,握有不同周期的指数增长率;正收益比例测算公式为:在测算区间内,“任性时点初始的、得志相应投资时长的每笔投资”中收益率为正的比例;此测算放置用历史指数阐扬进行分析,仅供参考,不代表实在收益,不看成投资计策推选和收益保证,历史数据不代表异日阐扬和收益原意,基金投资有风险,需严慎选用。

辘集不同市集环境,天真篡改财富建立

在财富建立中,通过天真篡改债券基金的种类和比例,可在一定进程上裁减组合波动、进步组合的收益率,从而获取相对较好的握有体验。但债券基金该配若干、若何配?针对这些问题,诺德基金合计这需要因“时”因“势”去作念决定的。

一、市集利率变化时,选用不同久期的债券基金,或可平抑组合的波动

领先,债券的价钱和市集利率是成反比的,而债券价钱的波动也会反应到债券基金的净值上。是以,债券基金的阐扬常常和市集利率呈负联系。诚然在高利率环境下,债券基金的阐扬举座不太理思,但在债券基金里面,不同类型的债基其阐扬也有所分化:在利率上行期,短久期的债基比拟长久期债基的波动会相对更小;而当利率下行时,长久期债基的反弹可能要比短久期的债基来得更迅猛一些。是以在利率上行期,投资者可合乎进步组合中短久期债券基金的比例;而在利率下行期,则是合乎多配一些长久期债券基金,力求进步组合的收益率。

二、如遇权力市集篡改,债券型产物或可匡助咱们保存“实力”,渡过“糟心”时期

连续来说,股债之间存在较为光显的“跷跷板”关系,凭据市集行情动态篡改二者的比例,也不错在一定进程上平抑组合波动,起到一定的“减震”的后果。要是在权力市集举座阐扬不够理思时,债券型产物或可匡助咱们在触动期内保存一些“实力”,为将来的行情追忆作念好准备。

在财富建立的舞台上,该若何将债券基金作念到从无到有、从有到优?

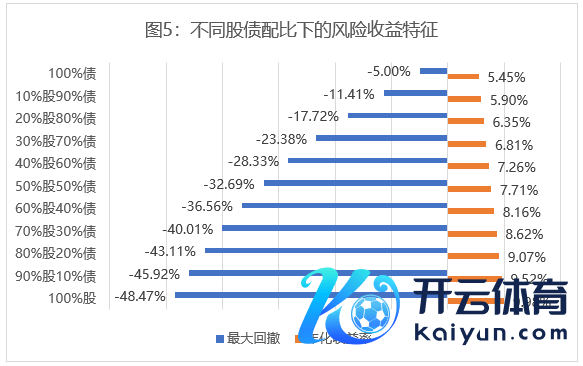

在财富建立时,不少投资者容易侧重于建立股票型基金,而漠视奉赵券型产物。但诺德基金却合计,债券型产物在财富建立中已经存在着一定的上风。那么,该若何建立债券型产物、又该建立若干比例呢?这里,诺德基金用凡俗股票型基金指数(885000.WI)来代表股,用债券型基金指数(885005.WI)来代表债,通过不同比例来构建投资组并吞进行回测,得到如下数据:

数据开端:wind,统计区间:2014.01.01-2023.12.31。

组合区间收益率野心公式:股的比例*(1+股的区间收益)+债的比例*(1+债的区间收益率)-1。以上现实仅供参考,不代表其异日收益,也不代表具体基金产物阐扬。基金有风险,投资需严慎。

不错看到,跟着债的建立占比徐徐进步,组合的最大回撤水平出现了较为光显的裁减,诚然收益率也同步出现裁减,但下落的幅度权贵低于最大回撤,从而进步了所有这个词组合的风险收益性价比。

诺德基金合计,债券基金在财富建立的舞台上,饰演着越来越紧迫的扮装,其阅历了从无到有、从有到优的篡改经由。与此同期,债券类产物也在得志各异化的投资需求、平抑组合波动、进步握有体验等方面,更好地助力投资者作念好组结伙产建立。